Rolling exogenous shocks to the economy have been growing of late but became the defining characteristic of the start of 2022. We spent the first few months of this year re-vising our interconnecting set of models that are foundational to our understanding of the course of the global energy transition. As so often, our suspicion is that the unforeseen secondary cross-sectoral effects from the energy price shock will turn out to have the greatest impact on our economy. A more holistic view is thus imperative to be able to spot investment opportunities when they arise.

Although at least superficially unrelated, we see poor governance as one commonality to today’s economic and geopolitical shocks, be it through over-stimulus of demand in the US in response to a supply-constraining pandemic, or via the EU’s historic reticence to balance the tension between climate ambitions and pragmatic reality. The zealot-like pace of closure of domestic hydrocarbon production serving unfortunately to have increased dependence upon Russian imports. At the root of this repeated governance deficit across so many stakeholders we see it is caused by suboptimal agency/principal behavioural incentives. Our main focus has been on the systemic implications and specific investment opportunities this presents for Europe and especially ESG.

As part of this analysis, we previously constructed a set of 20 interacting models to assess the carbon price required to incentivise each hard-to-abate industry to reach Net Zero by 2050. At the start of this year, we extended this work to analyse the consequences to global oil and LNG markets should Europe attempt to reduce its dependence on Russia gas imports and what this may mean for and between different European companies.

To summarise, our three main investment conclusions from this analysis are as follows:

- Energy efficiency is now a strategically supported industry: The most direct substitute to Europe’s dependence on Russia is for Europe to purchase more LNG. However, the size of the spot uncontracted global LNG market is only 150 Million Tonnes (MT) p.a., roughly equivalent to Russia’s gas exports into the EU. To reduce exposure to Russia, Europe would have to take a greater share of this limited resource from China amongst other Asian countries but may hold the weaker hand. Europe’s electricity system works by a mechanism in which the most expensive source of required marginal supply sets the wholesale price for all power. The price of LNG has more than doubled from $15 to $35/MMBtu and the economy must absorb an energy shock of €1.2 trillion or 7% of GDP. Reducing reliance on both Russia and LNG is therefore imperative and we think a substantial improvement in energy efficiency has become a continental-wide strategic priority. Indeed, the recent EU publication on this topic (RePowerEU, March 2022) stated an ambition to reduce gas consumption by 38 billion cubic meters (bmc) p.a. (25% of Russian imports) through accelerated investment in building efficiency (e.g. heat pumps, insulation) and energy management systems.

- Economics of electrification reaching inflection point: Even assuming some degree of normalisation, elevated hydrocarbon prices are accelerating the payback on switching to electricity-based alternative forms of production in many industries. For example, we show the increased attractiveness of electric versus Internal Combustion Engine (ICE) cars currently versus pre-shock and similarly the improved Levelised Cost Of Energy (LCOE) of renewable power generation versus fossil-based traditional alternatives. The electrification industry vertical has a number of niches in which supply-side incumbents offer inexpensive access to this optionality on accelerating demand and critically also benefit from persistently high entry barriers

- Picks and shovels to the investment in self-sufficiency: European self-sufficiency requires greater investment in energy, raw materials, defence and technology and the ‘pick and shovel’ providers to modernising the economy stand to benefit in our view. Given the extensive debt in the economy and scale of required expenditure, we think windfall taxes and encroaching regulation of perceived ‘non-productive’ profit generators will likely increase. Less aligned industries may prove vulnerable in our opinion as we saw already with EDF in France. In our view, this dynamic would seem to imply potential for share price performance bifurcation and thus be supportive prospectively of active rather than passive approaches to equity selection.

Europe’s age old problem of self-sufficiency

Taking a step back, Europe’s relative lack of energy resources, raw materials and land has influenced its economic and political development for centuries. The EU’s Ukrainian dilemma arising from over-dependence on Russian oil and gas is just a new version of an old problem. The industrial revolution may have originated in the region precisely as a consequence of such broad resource limitations, productivity thus being forced to play a more vital role in being able to generate economic added-value.

In some ways, Europe’s position in the vanguard of the drive towards ESG is a modern manifestation of a solution to the same time-honoured set of input constraints. Sustainable and efficient use of all factors of production offers the greatest marginal benefit in conditions where their relative abundance are amongst the most limited. Forced to survive within such a thrifty ecosystem, European corporates have developed silos of genuine global IP excellence in mechanical engineering (Scandinavia) and electrification engineering (France) whose capacity for added-value is likely to become more appreciated as ESG and Industry 4.0 shape the future industrial economy.

Rather than the underlying principles of ESG which we therefore think are sound, our issue has been the lack of pragmatism of political objectives and thus policies selected to implement them (e.g. the overly-ideological aversion to gas in the transition). The distortion to market signals unintentionally but paradoxically heightens the risk of failure to achieve the desired outcome.

It is possible that this historic lack of pragmatism will not greatly matter and going forward has now been rectified via crisis. Yet, independent of the outcome in Ukraine, it has become clear that Europe has become structurally over-reliant on Russian energy imports and is likely to implement the steps outlined in the RePower EU policy document to be able to disconnect totally by 2030.

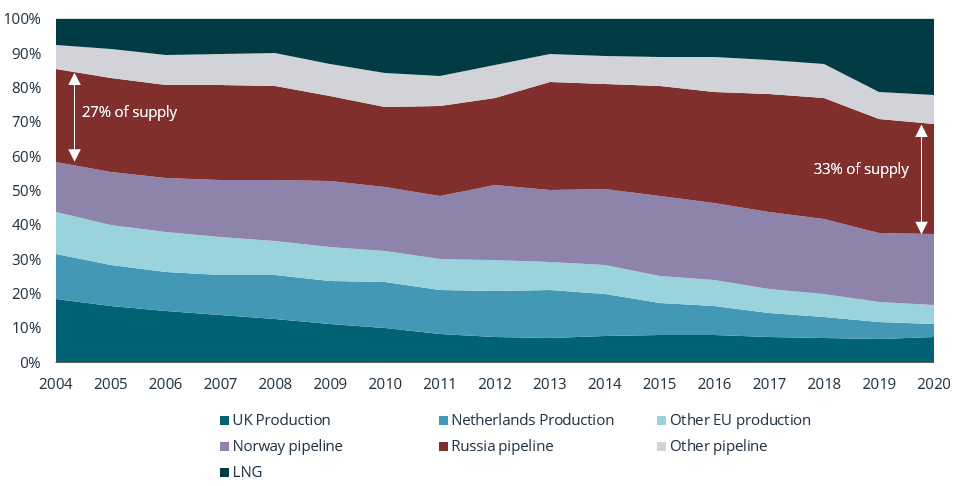

European Gas: Overly Dependent On Russia (EU Gas Supply By Source, %)

Sources: Eurostat, Lansdowne analysis

Understanding the impact from Europe’s de-coupling of Russia

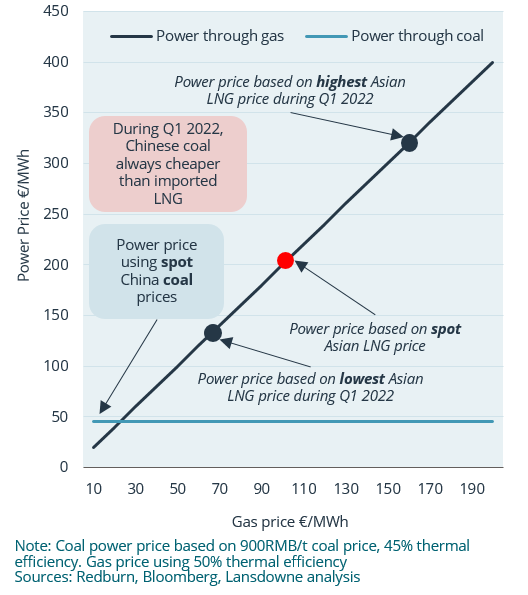

Under the RePower EU strategy, Europe seeks to substitute 50bcm p.a. (37MT) of Russian gas with global LNG imports by the end of 2022. The issue is that incremental demand from Europe would push this year’s global LNG market into deficit of about 7MT (or 2%) and probably also for each of the next three years. Additionally, within the LNG market, the size of uncontracted spot volumes at any point in time is actually quite a lot smaller at about 150 MT of the 400MT p.a. total with the rest unavailable due to pre-agreements. To achieve this year’s objective, Europe must take share of this constrained pool from other purchasing nations. China is the largest consumer of imported LNG at 80MT p.a. and could substitute this by increasing domestic coal production by 300mt p.a. or c. 5% of existing capacity. At currently very elevated levels of gas prices relative to coal, there is a strong economic incentive to do this but paradoxically, Europe’s ambitions towards net zero would then inadvertently have undermined China’s own efforts. Since China is a predominantly coal-centric economy, we estimate the impact of high gas prices are $50 billion p.a., or only 0.3% of GDP, and since the energy system is also state controlled, this is not being passed on directly to the consumer. This implies that China has the flexibility to prioritise its climate ambitions by continuing to purchase LNG if it so chooses making it imprudent for Europe to rely on LNG imports as a sustainable substitute to Russian gas in our opinion.

China: Strong Price Incentive Switch From Gas To Coal

China Power Prices Sensitivity To Gas Prices, €/MWh

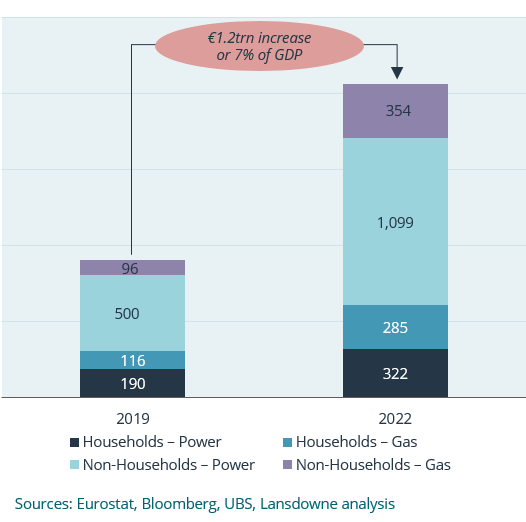

Separately, to analyse the potential increase in energy costs to the European economy, we have built a consumption model for the three principal end markets; heating, power and industrial, and by source i.e. gas, renewables and other. Compared to the pre-covid baseline of 2019, we estimate that Europe’s energy bill on a spot basis has increased by €1.2 trillion or 7% of GDP of which €300 billion for households.

The extent to which this will impact European GDP growth is still unclear as it is possible that factors outside of demand destruction can also induce energy prices to normalise. A ceasefire could encourage Russian exports to be re-accepted into the global system and other LNG importers like China may elect to switch to domestic substitutes and thus ease the pressure on the LNG market. Additionally, hedges and government support for energy poverty could also help to smooth the impact. Moreover, European households have accumulated c. €800 billion of excess savings versus pre-covid trend that could act as a shock absorber. During the two pandemic-impacted years of 2020-2021 and versus prior trend growth rate, EU household disposable income fell €500 billion but consumption shrank by an even greater €1,300 billion; thus savings increased by €800 billion versus what could have been expected.

EU Energy Shock: €1.2trn Cost Increase or 7% of GDP

2022 vs 2019 Estimated European Power and Gas Costs

Nevertheless, recent developments such as the above serve to reinforce the view that global real demand growth is likely to slow through the year. It seems overly optimistic under current conditions to presume that households will absorb elevated energy volatility and the resultant decline in real incomes by drawing down accumulated excess savings in order to continue growing consumption spend in line with pre-covid trends (i.e. 3-4% per year). Indeed, the second order consequences such as that from immigration and food shocks in North Africa and the Middle East represent additional tail risks to the global economy that also have to be considered. The violent move within equity markets into ‘value’ in the first quarter would seem to belie the breadth of potential economic environments that are now increasingly possible.

What seems most clear to us is that the combination of global fragmentation and the region’s climate ambitions will inject accelerated momentum into Europe’s transition towards greater energy efficiency and electrification. Russian gas is unreliable, LNG is expensive and the European consumer is stretched. At current oil and gas prices, the economic incentive for greater investment in the transition has leapt forward in time and it is plausible that European fiscal policy is additionally loosening.

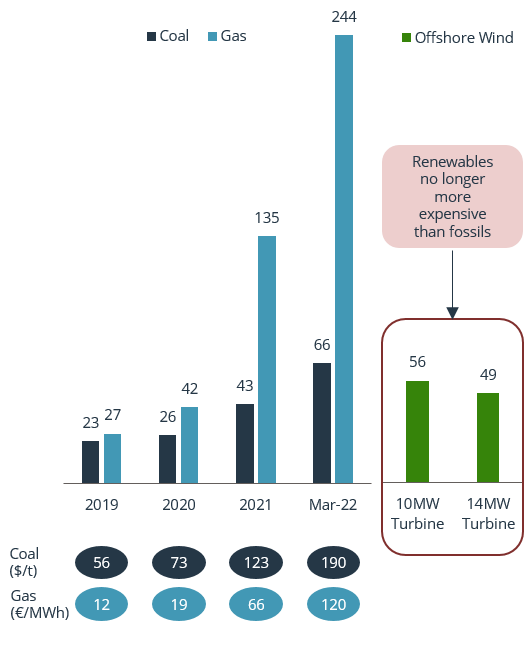

Given the explosion in coal and LNG prices, we calculate that it is now cheaper to generate power from offshore wind than from fossil fuels on an LCOE basis whereas it was 2x more expensive as recently as 2019. Critically, regulatory subsidies are thus no longer required for the economics to work. Similarly, the total cost of ownership of an electric vehicle at the consumer level is now 20% lower than for a car that runs on gasoline at current fuel prices, from nearly breakeven only two years ago. The inflection point at which the economic cost of switching to electrified and energy-efficient alternatives has moved into-the-money across a swathe of end markets.

Power: Renewables Now Competitive Vs Fossil

Levelized Cost Of Energy, €/MWh, excluding CO2 costs

Sources: Bloomberg, Lansdowne analysis, Siemens Gamesa, Orsted

Finding Investment Opportunities in Today’s Turbulent Europe

Current developments in energy markets may represent one strand of a greater trend towards de-globalisation. In the long run, reliance on Russia can be disintermediated but the sheer size and interdependence with China makes the latter a much more insoluble issue. It is too early to predict the full extent of any decoupling that may eventually in reality happen but each major global actor is incentivised to increase its internal self-sufficiency. This could well result in a period of re-investment in core factors of production including energy, raw materials, defence, healthcare and technology.

The substantial re-design of existing economic infrastructure would throw up a host of new investment opportunities as well as losers to avoid. A key question to us is the depth in reality of the current policy shift taking place in Europe. At present, we doubt there has been enough of a shunt forward to facilitate the creation of a pan-European banking industry but conversely think that chronic under-investment in defence will now be rectified. Oil majors seem the most difficult and dependant on time horizon. The shortage in supply and resultant high prices mean they are trading on cash flow yields we have never seen before. Yet the acceleration in renewables, electrified mobility and hydrogen investment suggest peak demand is only circa five years away (our model available to clients upon request) and in the long-run, prices may fall precipitously as the coalition of producers dissolves as each attempts to minimise its own stranded assets.

Like the oil majors, we think obsolescence represents a risk for diversified miners particularly with respect to Platinum Group Materials used in ICE automobiles, diamonds that can be synthesised as well as metallurgical coal and iron ore as steel manufacturing moves to hydrogen with DRI EAF technology from traditional blast furnaces. A wave of M&A is likely in our view as the large caps try to increase aggregate exposure to new economy metals given the paucity of organic growth opportunities. We are particularly interested in the potential development of infrastructure for secondary supply as a potential alternative for economies like Europe to reduce its over-dependence on imports of expensive virgin raw materials. We think that recycling is going to deepen within existing areas of activity and broaden to include a widening array of inputs over coming years.

Further downstream, utilities appear a likely beneficiary of energy deficits but here it must be acknowledged that this is accompanied at present by limited visibility on terminal value. We think Europe will move to decouple the price mechanism for electricity generation from that of the gas market and thereby shift from a merit order to a payment for capacity model. In theory, the certainty such volume contracts bring could be very valuable but greater administration of energy markets carries its own sizeable risks as demonstrated by developments at EDF in France this quarter.

Rather, we continue to prefer the ‘pick and shovel’ providers that are required in the modernisation and raising self-sufficiency of the economy but are far from the government and less regulated. We invite the reader to get in contact to discuss our further thoughts on this topic.

Disclaimer: The views expressed herein are the views of the European Long Only team and not necessarily of Lansdowne Partners (UK) LLP as a whole. The content of this Article has been prepared by the European Long Only team alone and is not, and has not been endorsed or approved by any other person. The article and the information, statements, opinions, interpretations and beliefs contained in it are those of the European Long Only team and are provided in good faith, but no representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the contents of the Article, and no person shall be entitled to place any reliance on the Article or its contents. This Article is not intended to be, nor should it be construed as, investment, financial, tax or legal advice, or a recommendation to buy, sell or hold any security or other investment or pursue any investment strategy. Neither this letter nor any of its contents constitutes an inducement, offer or solicitation to purchase or sell any securities.

More Insights

Peter Davies, Head of Developed Markets Strategy at Lansdowne Partners, has written a timely article on the UK growth debate, challenging some of the more widely held assumptions about the current state of the economy.

19 June 2026

Daniel Avigad reconnected with Andrew Van Sickle to unpack European equities, growth challenges and the impact of populism.

1 April 2026

In a Trustnet article, Daniel Avigad, Portfolio Manager of the Lansdowne European Strategy, spoke with Emmy Hawker to unpacks how Europe’s fragmented governance is holding back its push for true strategic autonomy and why rising political, market and geopolitical pressures could create opportunities for investors.

23 February 2026